Index Linked Gilts: The advantages for high income clients

12 April 2023

This tax-year end, my postman commented on the increased volumes of paperwork sent to my house, with pretty much anyone I’ve ever dealt with mailing me about using my SIPP and ISA annual allowances. How relevant are these annual limits going forwards, especially following the scrapping of the lifetime allowance in the Budget?

Annual Limits

There are still some annual limits which may impact high net worth clients. For example, those that have begun flexible withdrawal from their pension will be affected by the money purchase annual allowance (MPAA). Although this is increasing from £4,000 a year to £10,000 this month, it is still significantly lower than the new ‘normal’ pensions annual allowance of £60,000.

There are still some annual limits which may impact high net worth clients. For example, those that have begun flexible withdrawal from their pension will be affected by the money purchase annual allowance (MPAA). Although this is increasing from £4,000 a year to £10,000 this month, it is still significantly lower than the new ‘normal’ pensions annual allowance of £60,000.

In addition, those with ‘adjusted income’ in excess of £260,000 are subject to the tapered annual allowance (TAA). So, if a member’s adjusted income is over £260,000 in the upcoming tax year, their annual allowance may be reduced. For every £2 it goes over £260,000, their annual allowance for the tax year will reduce by £1. Their annual allowance can drop to the new minimum TAA of £10,000 (increased from £4,000).

Those with high income caught by this restriction may have to reduce the contributions paid by them and/or their employer, or an annual allowance charge will apply. Of course, it is still possible to carry forward unused annual allowance from previous years to a year where the taper applies.

Meanwhile, Isas remain a highly tax efficient and versatile home for non-pension investments. But they have a strict £20,000 annual limit and, unlike pensions, this limit cannot be exceeded. The latest distributional analysis by HM Revenue & Customs, from the 2019/20 tax year, shows that 1.8 million people maxed out their Isas with a full £20,000 contribution. It’s a fair guess that quite a lot of them still had money left over they have had to invest elsewhere.

Part of the attraction of both pensions and Isas is that investments are shielded from both income tax and capital gains tax (CGT). However, what if there was an investment that paid almost no income, was exempt from CGT and could still be held on platform within your clients’ general investment account (GIA)?

Index Linked Gilts

Such an investment is UK index-linked gilts. There are multiple upsides of buying index linked gilts right now, which may make them worthy of consideration for inclusion in client portfolios:

- The investment will grow in line with the highest accepted measure of inflation – the UK Retail Price Index (RPI) – and will only switch to the lower Consumer Prices Index (CPI) from April 2030. RPI was running at 13.4% in January.

- The investment can be for as long as you like, as maturity dates for individual gilts are pre-selected. They run up to 2073 – 50 years from now.

- Prices for index linked gilts fell heavily in the liability-driven investment (LDI) crisis that enveloped Liz Truss’s short-lived premiership last autumn. Many have stayed below par, meaning that on maturity not only will clients get back their original investment plus inflation, but also benefit from a capital uplift.

- Dividend payments on index linked gilts are set extremely low, with many paying just one-eighth of 1% per annum. These dividends are liable for income tax, but this level of income renders their tax implications almost negligible.

- Capital gains on investment in linkers are tax free. Bear in mind, at the same time, the CGT free allowance is falling fast: in tax year 2024/25 the CGT allowance will have fallen to just £3,000 from £12,300 in the current tax year.

- While individual index linked gilts have a fixed end date when the government must redeem them, your client can readily sell them in the market before then. Early sale does not endanger that important ‘CGT-free’ benefit. Selling early could be useful if clients’ needs change or could simply be opportune if the price of linkers goes back up again as the UK gradually rebuilds its reputation for safe money policies that former chancellor Kwasi Kwarteng so spectacularly destroyed.

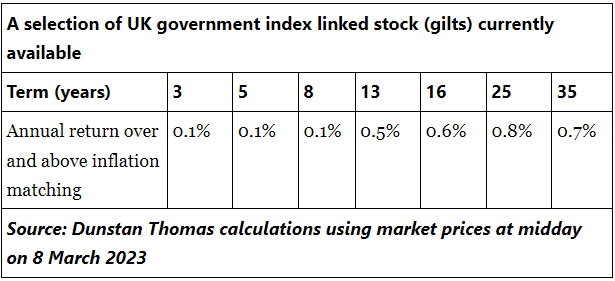

The relatively high cost of government borrowing, combined with their tax advantages and inflation protection, could mean buying index linked gilts within a GIA is worthy of consideration for clients who have maxed out both their pensions and Isas. Here is a selection of different length index linked gilts, together with the real yield they offer over and above inflation:

Previous Article

Dunstan Thomas Products

Contact Us

Previous Article

Dunstan Thomas Products

Contact Us

Adrian Boulding

Director of Retirement Strategy at Dunstan Thomas

023 9282 2254

enquiries@dthomas.co.uk